Why do we Show a Loss on our Financial Statements When we Paid for Things out of our Reserves?

It can be confusing when you pay expenses out of your reserves yet see a loss on your financial statements.

It helps to think about the accounting entries to record the expense and transfer from reserves and its effect on your financial statements.

A reserve is usually a board or management-designated unrestricted fund set aside as a “rainy day fund” meant for temporary cash flow issues, unexpected expenses, or to launch new programming. It is common for the stakeholders who built the reserve to want to be able to show the transfer from the reserve as "revenue" to cover the expense.

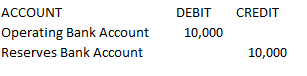

FUNDS TRANSFER

In practice, you would likely move funds from the reserves account to the operating account (below), and then pay from the operating account as noted above. This does not create revenue.

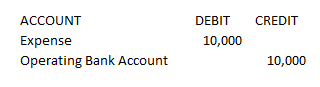

EXPENSE

When you have a normal expense, you enter the expense as reducing a bank account, like your operating account, with the following entry:

The entry increases expenses on the statement of activities (income statement, profit & loss) and decreases the operating account balance on the statement of financial position (balance sheet). The expense increase, if larger than revenues, can cause negative net assets, or a loss, for the reporting period.

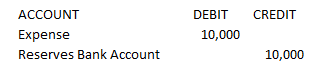

Let’s look at the entry if you pay for the expense from reserves.

Swapping the operating bank account for the reserves bank account leaves the effect on the financial statements unchanged. The account you use to pay for the expense doesn’t change the result; a loss on the statement of activities occurs if expenses exceed revenue.

It is possible to include a note in internal financial statements noting that the deficit that appears on the financial report is being covered by the reserves, however, it is important that it is clear that the external-facing financials will show a deficit when funds are spent from reserves.